© Export Finance Australia

The views expressed in World Risk Developments represent those of Export Finance Australia at the time of publication and are subject to change. They do not represent the views of the Australian Government. The information in this report is published for general information only and does not comprise advice or a recommendation of any kind. While Export Finance Australia endeavours to ensure this information is accurate and current at the time of publication, Export Finance Australia makes no representation or warranty as to its reliability, accuracy or completeness. To the maximum extent permitted by law, Export Finance Australia will not be liable to you or any other person for any loss or damage suffered or incurred by any person arising from any act, or failure to act, on the basis of any information or opinions contained in this report.

Bangladesh—Smooth election but ongoing risks to reform momentum

Bangladesh held national elections on 12 February, the first since a student-led uprising ousted long time autocrat Sheikh Hasina. The Bangladesh Nationalist Party (BNP), led by Tarique Rahman, secured 209 out of 300 parliamentary seats, while Jamaat-e-Islami became the main opposition with 68 seats after campaigning on a moderate policy platform. The newly formed student-led National Citizen Party won six of the 30 seats it contested. Sheikh Hasina’s Awami League party was banned from participating. A smooth transition of power from the technocratic interim leader, Muhammad Yunus, who stepped in after the uprising in mid-2024, is expected. Voters also delivered support for the ‘July Charter’ (a suite of constitutional reforms) to strengthen Bangladesh’s democracy, including introducing a bicameral legislature and term limits for prime ministers. The newly sworn-in Parliament will be responsible for enacting the July Charter, but the BNP lodged a series of objections to aspects of the Charter pre-election.

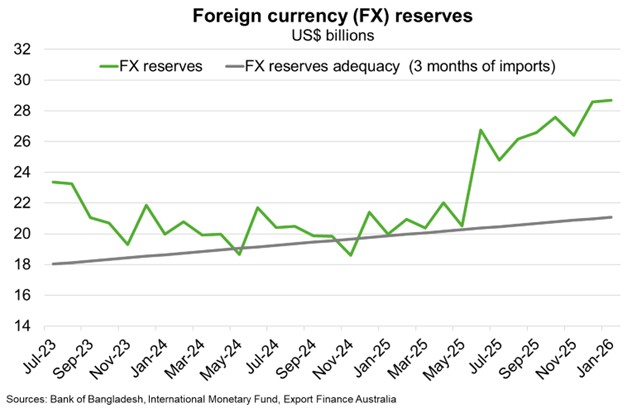

Alongside the July Charter, the interim government pursued economic governance reforms to address systemic weakness in the banking sector and an unsustainable foreign exchange (FX) regime. FX reserves have rebuilt from inadequate levels in 2024 (Chart) with implementation of some IMF-mandated reforms and solid remittance flows. However, continued IMF-led reform progress is essential for Bangladesh’s ongoing social and economic stability. Any lost reform momentum could see FX levels return to critically low levels hampering importers’ ability to pay for goods and services in international currencies. Bangladesh is scheduled to graduate from Least Development Country (LDC) status, but the BNP is seeking a deferral of at least three years to extend preferential market access to major export markets. On the upside, Bangladesh is likely to benefit from the equalization of its US tariff rate with competitors, initially through a trade deal announced on 5 February (lowing its tariff to 19%) and subsequently the US Supreme Court striking down International Emergency Economic Powers Act tariffs. Bangladesh now faces the same tariff as most of its competitors in its largest export market; 15% on most imports under Section 122 of the Trade Act of 1974.